.png)

Klarna vs Afterpay: Which Buy Now, Pay Later Option is Right for You? (2024)

Buy now, pay later (BNPL) services have become increasingly popular in recent years, as they offer a convenient way to spread out the cost of a purchase over time. Two of the most popular BNPL services are Klarna and Afterpay.

Thinking about Klarna or Afterpay, what to choose?

Well, BNPL service apps like Klarna and Afterpay both offer similar services, allowing users to make a purchase now and pay for it in installments over a period of weeks or months. However, there are some key differences between Klarna and Afterpay.

In this blog post, we will compare Klarna and Afterpay in detail, so you can decide which one is right for you.

What is Klarna

Klarna is a Swedish financial technology company that provides e-commerce payment solutions. The company was founded in 2005 by Sebastian Siemiatkowski, Niklas Adalberth, and Victor Jacobsson. Klarna is headquartered in Stockholm, Sweden, and has offices in 20 countries around the world.

What is Afterpay

Afterpay is an Australian buy-now-pay-later (BNPL) company that allows customers to make a purchase now and pay for it in four installments over six weeks. The company was founded in 2014 by Nick Molnar and Anthony Eisen and is headquartered in Sydney, Australia. Afterpay is available in Australia, New Zealand, the United States, the United Kingdom, Canada, and France.

Klarna vs Afterpay: Features

Klarna and Afterpay are both popular "buy now, pay later" (BNPL) services that allow consumers to make online purchases and pay for them in installments. Here's a comparison of their features:

Klarna features

- Shopping Experience: Klarna offers a seamless and user-friendly shopping experience like Manifest AI with a "Pay Later" option at the checkout, allowing customers to split their payments into four equal installments.

- Global Reach: Klarna is available in multiple countries and has partnerships with a wide range of online retailers, making it accessible to a global audience.

- Klarna App: Klarna provides a dedicated app that allows users to manage their purchases, track deliveries, and make payments conveniently.

- Pay Later and Financing Options: In addition to the "Pay Later" option, Klarna offers financing plans with longer-term options, including interest-free periods and fixed-term financing.

- Rewards Program: Klarna offers a loyalty program called "Vibe" that provides users with rewards, exclusive deals, and discounts from partner retailers.

- Return Protection: Klarna's "Pay Later" feature allows customers to receive refunds for returned items, helping to simplify the returns process.

Afterpay features

- Installment Payments: Afterpay allows customers to split their payments into four equal installments, with payments due every two weeks. The service is available at the checkout of various online retailers.

- Late Fees: Afterpay charges late fees for missed payments, which can vary depending on the total purchase amount and the country's regulations.

- Online Marketplace: Afterpay offers a marketplace feature called "Shop Directory," where users can discover and shop at participating online stores.

- App Integration: Afterpay has a mobile app that allows users to manage their payments, view upcoming payment schedules, and access exclusive offers from partner merchants.

- Credit Checks: Afterpay typically performs a soft credit check during the application process, which doesn't impact a user's credit score.

- No Interest: Afterpay doesn't charge interest on its installment payments; however, late fees may apply for missed payments.

Afterpay vs Klarna: Pricing & Plans

Klarna and Afterpay are two of the most popular buy now, pay later (BNPL) services. Both services offer a similar payment plan, allowing customers to make a purchase now and pay for it in installments over a period of time. However, there are some key differences between the two services in terms of pricing and plans.

Klarna pricing

- Pay in 4: This option allows customers to make a purchase now and pay for it in four installments over six weeks. There are no interest or fees if the installments are paid on time.

- Slice it: This option allows customers to make a purchase now and pay for it over a longer period of time, up to 36 months. Interest rates vary depending on the purchase amount and the length of the repayment period.

- Pay in 30 days: This option allows customers to make a purchase now and pay for it within 30 days. There is a late fee of $7 if the payment is not made on time.

Afterpay pricing

- Four installment payments: This option allows customers to make a purchase now and pay for it in four installments over six weeks. There are no interest or fees if the installments are paid on time.

- Monthly installments: This option allows customers to make a purchase now and pay for it over a longer period of time, up to 12 months. There is a late fee of $10 if the payment is not made on time.

Klarna Vs. Afterpay Pros & Cons

Klarna and Afterpay are two of the most popular BNPL services, and they both have their own pros and cons. Here is a comparison of the two services:

Klarna Pros & Cons

Pros:

- No interest or fees if installments are paid on time

- Available at over 250,000 merchants

- Offers a variety of payment plans, including Pay in 4, Slice it, and Pay in 30 days

- Offers a virtual card that can be used online and in-store

- Offers a mobile app that makes it easy to track payments and manage your account

Cons:

- Can lead to overspending if not used responsibly

- May not be available to everyone

- Can affect your credit score if you miss a payment

Afterpay Pros & Cons

Pros:

- No interest or fees if installments are paid on time

- Available at over 100,000 merchants

- Offers a simple and straightforward payment plan

- Does not conduct a hard credit check when you sign up

- Offers a mobile app that makes it easy to track payments and manage your account

Cons:

- Can lead to overspending if not used responsibly

- May not be available to everyone

- Can affect your credit score if you miss a payment

Overall, both Klarna and Afterpay are good BNPL services with their own pros and cons. The best service for you will depend on your individual needs and preferences.

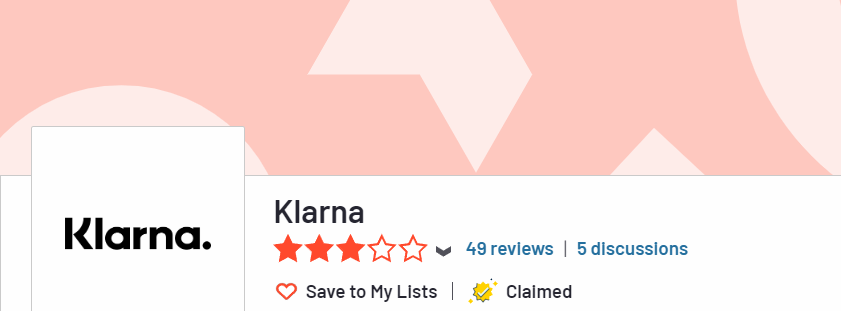

Klarna reviews

Klarna has a rating of 4.2 out of 5 stars on Trustpilot, based on over 1 million reviews. Here are some of the things that customers like about Klarna:

- The ability to make purchases now and pay for them later without interest or fees.

- The convenience of using Klarna online and in-store.

- The easy-to-use mobile app.

- The flexible payment options.

- The customer service.

Here are some of the things that customers dislike about Klarna:

- The late fees can be high.

- The credit check can affect your credit score.

- Not all merchants accept Klarna.

- The app can be buggy sometimes.

Afterpay reviews

Here are some reviews of Afterpay by customers:

"I love Afterpay! It's so convenient to be able to buy something now and pay for it later. I've never had any problems with the service and I always get my payments on time."

**"Afterpay is a lifesaver! I'm a student and I don't always have the money to buy things outright. With Afterpay, I can spread out the payments and make it more affordable."

**"I've been using Afterpay for a few months now and I've been really happy with it. The app is easy to use and the payments are always on time. I would definitely recommend it to anyone looking for a BNPL service." \

Klarna Vs Afterpay: Which is best for an e-commerce business?

Check the factors to decide the best for an ecommerce store:

Payment Options

Klarna and Afterpay both offer customers the ability to split their payments into manageable installments. Klarna provides a "Pay Later" option with four equal payments, while Afterpay offers a similar four-payment plan. Neither service typically charges interest on these installments.

Late Fees

Both platforms may impose late fees if customers miss a payment. It's crucial to understand the specific fee structure and terms associated with late payments for each service. Ensure your customers are aware of these potential charges.

Geographic Availability

Consider the geographic reach of each platform. Klarna is available in multiple countries, making it suitable for businesses with an international customer base. Afterpay may have limitations in terms of the regions it serves.

Integration

Evaluate how seamlessly each service integrates with your e-commerce platform. The ease of implementation and user experience can vary between Klarna and Afterpay, so choose the one that aligns with your existing systems and workflows.

Customer Experience

Think about your customers' preferences. Some shoppers may prefer Klarna's interface and features, while others may find Afterpay more appealing. Understanding your target audience can help you make the right choice.

Marketing Support

Consider any additional marketing support or promotional opportunities that Klarna or Afterpay may offer to e-commerce businesses. These can include co-branded campaigns, discounts, or special promotions that can help boost sales.

Klarna vs Afterpay: Alternatives

Several alternatives to Klarna and Afterpay in the "buy now, pay later" space include:

- Sezzle: Allows customers to split payments into four interest-free installments with a focus on affordability.

- Affirm: Provides point-of-sale financing with various term lengths and interest rates, giving customers flexibility.

- PayPal Pay in 4: PayPal's installment solution offers a seamless checkout experience with four equal payments.

- Zip Pay: Allows customers to split payments into four interest-free installments, making online shopping more accessible.

- Splitit: Offers installment plans without the need for credit checks or applications, enhancing the buying experience.

- Shop Pay Installments: Offers installment plans powered by Shopify for seamless integration with e-commerce stores.

How Are Klarna and Afterpay Similar?

Klarna and Afterpay are both buy now, pay later (BNPL) services that allow customers to make a purchase now and pay for it in installments over a period of time. They are both popular with millennials and Gen Z consumers, and they are both accepted by a wide variety of merchants.

Here are some of the similarities between Klarna and Afterpay:

- No interest or fees if installments are paid on time: Both Klarna and Afterpay do not charge interest or fees if the installments are paid on time. This makes them a more affordable option than credit cards, which often charge high interest rates.

- Available at a wide variety of merchants: Both Klarna and Afterpay are accepted by a wide variety of merchants, including both online and in-store retailers. This makes them a convenient option for consumers who want to shop at their favorite stores.

- Popular with millennials and Gen Z consumers: Both Klarna and Afterpay are popular with millennials and Gen Z consumers. These generations are more likely to use BNPL services than older generations, as they are more accustomed to using technology and are more likely to be concerned about overspending.

- Offer a mobile app: Both Klarna and Afterpay offer a mobile app that makes it easy to track payments and manage your account. This is a convenient way to keep track of your BNPL purchases and make sure that you are making your payments on time.

Which is better Klarna or Afterpay?

Determining whether Klarna or Afterpay is better depends on various factors, including your business's specific requirements, geographic reach, and the preferences of your customer base. It's recommended to carefully assess both platforms' features, pricing, and integration capabilities before making a decision that best suits your e-commerce needs.

Conclusion

In comparing Klarna and Afterpay, it's clear that both offer similar "buy now, pay later" solutions, allowing customers to split their payments without interest charges. While the core concept remains the same, the choice between them may come down to individual preferences, retailer partnerships, and geographic availability. Customers should consider factors such as late fees, payment flexibility, and the specific terms offered by each platform when deciding which one aligns better with their needs. Ultimately, both Klarna and Afterpay provide convenient ways to manage payments, making online shopping more accessible and flexible for consumers.

FAQs

Here are some frequently asked questions related to Afterpay and Klarna

Is Klarna and Afterpay the same company?

No, Klarna and Afterpay are not the same company. They are separate and competing "buy now, pay later" service providers, each with its own set of features and offerings.

Is Klarna or Afterpay are better than Paypal?

Klarna, Afterpay, and PayPal offer different payment solutions, and the choice depends on individual preferences and business needs.

- Klarna and Afterpay: These are "buy now, pay later" services, providing flexibility with installment options. They may charge late fees and perform credit checks.

- PayPal: PayPal offers a wide range of payment options, including PayPal Credit for financing. It doesn't charge late fees but may have interest rates.